Is Birmingham a Digital Hotspot?

Birmingham has designated itself as a Smart City and at the core of any smart city is its strength in the Digital economy. This post explores how the city compares to elsewhere in the UK and what is being done to strengthen this increasingly important economic sector/ engine for growth.

There are a number of stimuli for this post. Firstly there is the view from David Hardman CEO of Innovation Birmingham that there is great strength in the digital sector, he quotes 3000 companies with a Birmingham postcode; it is just in his view we do not have the confidence to brag and market the city enough. This he has compared to the hype that surrounds East London. Secondly and a real driver behind this piece is the report produced by TechCityUK¹ called ‘TechNation Powering the Digital Economy 2015’ that looks at the strength of the UK’s Digital economy. And the tipping point, thirdly was I received recently the annual report from Digital Birmingham outlining much of the good work that has happened recently.

The TecNation report describes a thriving and rapidly growing sector with just over 47,000 companies nationally and employment levels at almost 1.5 million people in the UK; with employment forecast to grow by 5.4% by 2020. The sector has a GVA of £119bn and employs 7.5% of the British workforce. So it is definitely a sector that Birmingham should take seriously.

The TecNation report describes a thriving and rapidly growing sector with just over 47,000 companies nationally and employment levels at almost 1.5 million people in the UK; with employment forecast to grow by 5.4% by 2020. The sector has a GVA of £119bn and employs 7.5% of the British workforce. So it is definitely a sector that Birmingham should take seriously.

So looking at TechNation…what is the good news on Birmingham? Key points include;

- There was a 51% increase in new Digital companies incorporated between 2010-2013 in the City

- New companies formed in 2013/2014 represented 14% of the total cluster size

- 20,064 people are employed in the sector

So Birmingham has a significant and growing digital economy…but how does it compare with other clusters across the UK. The TechNation report covers this in detail.

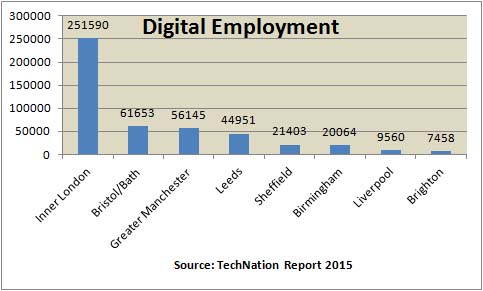

It found that Birmingham had only the 12th largest digital cluster by size of employment; behind a number of smaller places including Leeds who were 5th largest with almost 45,000 people employed and Bristol and Bath who were 2nd with just over 61,000 employees. By far the largest cluster was Inner London with employment of over 250,000. But what about growth levels. Well again Birmingham does not perform brilliantly, in the increase in companies incorporated between 2010-2013 and in terms of the 2013/2014 performance Birmingham was just below average on both measures.

The figure above shows the relative size of Birmingham’s digital employment and the task ahead; although there are some issues with the geography that I will touch on later.

The report brands the digital cluster as ’emerging’ with strengths in amongst other areas education technology and software development. There are also important initiatives under way that will really stimulate the sector.

- Digital Birmingham’s Annual report indicates take up by 907 firms of their Superfast Broadband grant. This has been extended to 2016..

- There is now a City Centre free wifi and over 200 Council buildings with public access now have free wifi.

- A new Greater Birmingham Digital academy has been created by the Greater Birmingham and Solihull LEP to focus on Digital skills in SMEs³

- The Innovation Birmingham project ICentrum; recently shown to George Osborne is exactly the right sort of investment that is needed. This £8m² project will create 400 high-value skilled tech. jobs, generating £25 million of GVA to the local economy per annum.

- The proposed Tech Enterprise Zone announced in last years Birmingham City Council Leaders Annual Policy Statement; if it comes to fruition could be another major boost.

In addition to these announced initiatives there are real plans to link these emerging digital strengths to the manufacturing economy through separate plans for Maker Spaces at Innovation Birmingham and in Digbeth being promoted by Eastside Projects.

But more needs to be done to maximise this growth and there are reasons for further action. The TechNation report details briefly the results from a survey they undertook of 2000 digital companies in the UK. In the view of these companies Birmingham had above average strengths in availability of property, access to transportation infrastructure and access to finance however it had a really negative element which was the perception by these companies of the region.

But it shouldn’t just be in a targeted Marketing Birmingham campaign; it needs to be much wider. We are a Smart City perhaps we need a Smart City Conference? Amsterdam promotes itself as a Smart City and at this moment a big international conference on Smart Cities is being hosted by the city. Similarly Barcelona does likewise. We seem to think marketing is a few banners on poles in the City Centre; and a digital presence but it is much more. We need as well to shout out about our centres of Digital economy; notably Innovation Birmingham, Digbeth and the Jewellery Quarter and further afield in the city region. Why not have a Digital Digbeth festival? What ever else David Hardman is right we need a more co-ordinated approach to marketing our Digital strengths.

Now lets look at some of the base data to try and get a Greater Birmingham picture. I didn’t have the time/skills to look at the employment figures – but TechNation with their partner Duedil have put up the company information on line by NUT3 geography – here and this makes interesting analysis. I added up what one might consider the core of the city region, namely the Black Country, Birmingham, Solihull and Coventry to get figures for ‘Greater Birmingham’

This shows a much more balanced picture than the employment figures quoted in the report. Interestingly for the hype around East London – West London just shades in terms of numbers of digital companies and taken together Inner London dominates the UK. However Greater Manchester is still in the lead of the other areas but only by approximately 20% from Bristol and Bath and Greater Birmingham. So in taking into account what is called our functional economic area we have a far greater number of Digital Companies than in Leeds for instance but its relative importance in Leeds given its smaller size is much more significant than in Birmingham.

This shows a much more balanced picture than the employment figures quoted in the report. Interestingly for the hype around East London – West London just shades in terms of numbers of digital companies and taken together Inner London dominates the UK. However Greater Manchester is still in the lead of the other areas but only by approximately 20% from Bristol and Bath and Greater Birmingham. So in taking into account what is called our functional economic area we have a far greater number of Digital Companies than in Leeds for instance but its relative importance in Leeds given its smaller size is much more significant than in Birmingham.

This can be shown illustrated by looking at Birmingham and Leeds. Leeds according to the report has fewer companies but over twice the level of employment than in Birmingham (Not Greater Birmingham) where they have a similar number of firms as Birmingham but twice as much employment.

How can this difference in employment figures compared to numbers of Digital Companies be explained. It could be that Birmingham has a greater number of small companies with few employees. It could also be that there are greater numbers of ‘digital occupations’ working work for non digital companies in places like Leeds as the two sets of figures come from different data sets.

Using these figure if we extrapolate the relationship between numbers of companies and employment found in Birmingham to Greater Birmingham – this would imply a Digital employment number of potentially on a par with Leeds but still significantly behind Greater Manchester and Bristol/Bath.

So summarising (and correcting) the report on the face of it Greater Birmingham in terms of numbers of companies is a significant digital engine for the UK. In terms of employment it is less clear but if my rough estimates are anywhere near correct it is equally important in employment terms. It doesn’t challenge Inner London or yet Manchester but against other areas it stands its ground. If I were Digital Birmingham I would ask TechNation/Duedil to redo the analysis for Greater Birmingham in terms of employment and company growth to confirm this.

Obviously as well it has the seeds to become an even more significant ecosystem; if some of the myriad of smaller companies can grow then the City Region could indeed challenge Manchester. Greater Birmingham has got real strengths and it needs to keep on investing in this sector,and needs to market itself far more effectively for it to access more of these new jobs. Yes and by the way lets have much more data and thinking at a city region level!

[…] Nation Report it falls into the trap of looking solely at Birmingham. However, by adjusting to a Greater Birmingham focus this shows that outside of London, Birmingham vies with Bath and Bristol in the size of its tech […]